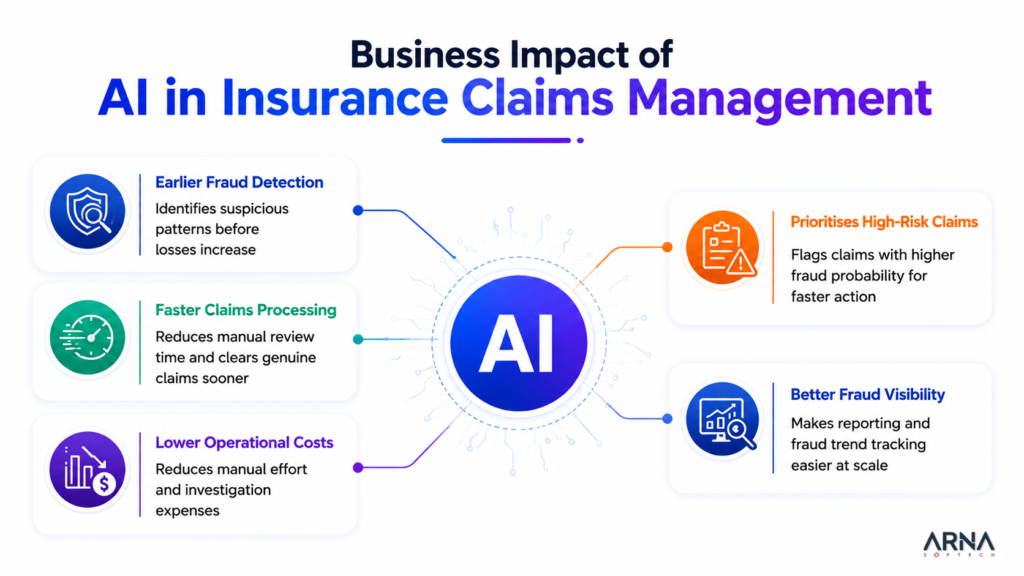

Insurance fraud isn’t new, but the scale of it today is. False claims cost the industry around $308 billion annually in the U.S. The manual way of catching it can’t keep up anymore.

Insurers are buried in paperwork and backlogs stretch for weeks. All because no human team can analyse thousands of claims at once. AI solutions are now filling this gap. They’re giving insurers the speed and accuracy to fight fraud and process claims without burning through resources.

Why Insurance Companies Are Adopting AI Solutions?

AI can check large volumes of structured and unstructured data to mark fraud cases. As claim volumes grow, AI helps insurers investigate more cases without delaying genuine claims or increasing pressure on internal teams.

How We Built an AI Solution to Detect Fraud More Efficiently?

One of our insurance clients was dealing with a growing claims backlog because most reviews and fraud checks were done manually. They received around 500 new insurance claims every day. Existing claims kept piling up as manually processing 2,000 claims took at least 7 days, creating delays in investigations and approvals.

To solve this, we built a custom AI solution that processed large volumes of insurance claims data and flagged claims most likely to be fraudulent, helping teams focus on priority cases faster. Here’s how it worked:

AI-Powered Fraud Detection Workflow

1. AI Automated Workflow Triggered

Every night, the system automatically starts processing all claims received during the day.

2. Claims Imported from Existing Claims Portal

Claims filed on an external portal are redirected to the client’s server for analysis.

3. Structured + Unstructured Data Collected

The system gathers all related claim information, including:

• Accident photos

• Agent and customer notes

• Investigation records

• Conversations and feedback

• Supporting documents

• Raw text data

4. Business Rules Applied

Predefined rules check policy details, claim conditions, verification criteria, and known fraud indicators.

5. LLM Analyses Claim Data

The model reviews data to spot anomalies or suspicious patterns.

6. Fraud Confidence Score Generated

Each claim gets a confidence score. Hence Higher score = Higher likelihood of fraud.

7. Claims Above Threshold Flagged

Claims crossing the defined cut-off are marked as potentially fraudulent.

8. Final Outcome

Detecting just 20 potentially fraud claims could help avoid losses of up to $260,000.

Conclusion

Custom AI development isn’t optional for insurers anymore. It’s quickly becoming the baseline. The question is less whether to adopt it and more how to do it right. Good AI consulting is what bridges the gap between a generic tool and something that fits your insurance operations.

Need support with AI adoption? Arna team is here to help.

Also Read: 5 Steps to Build a Successful AI Adoption Strategy

Frequently Asked Questions (FAQs)

How Can AI Be Used in Insurance?

Routine tasks take up a lot of time for insurers. AI helps save time here. Areas like claims review, fraud screening, and customer care are made simpler by AI.

What’s Next for AI in Insurance?

AI can create dynamic policies that adapt based on real-time behaviour. It can also automate complex legal and compliance reviews.

Can AI Do Insurance Underwriting?

Yes. AI can support underwriting by analysing large volumes of customer, policy, and risk data to speed up evaluations.